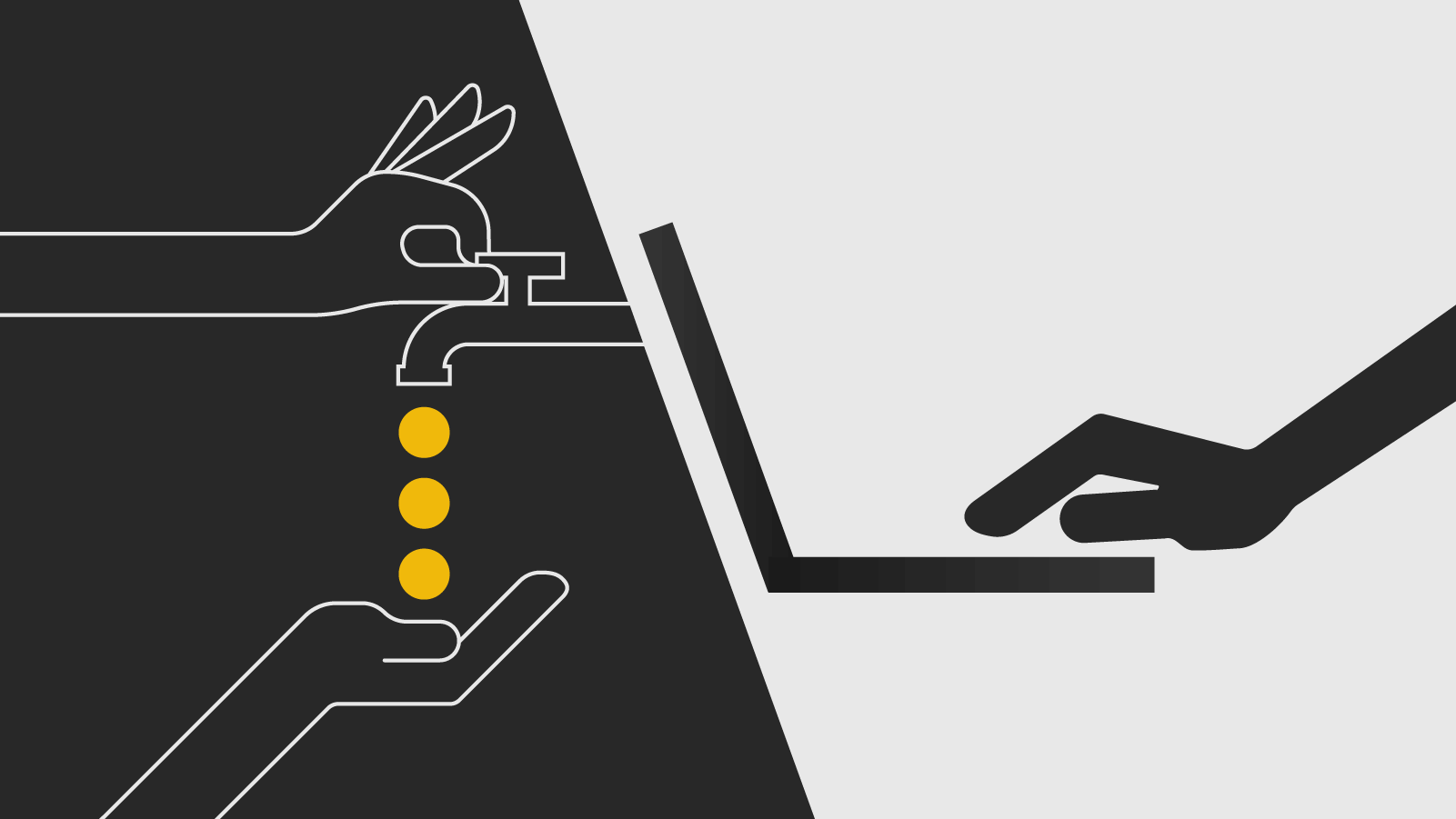

Fractional reserve is a banking system that allows commercial banks to profit by loaning part of their customers’ deposits, while just a small fraction of these deposits are stored as real cash and available for withdrawal. Practically speaking, this banking system creates money out of nothing using a percentage of their customers’ bank deposits.

In other words, these banks are required to hold a minimum percentage (a fraction) of the money that is deposited in their financial accounts, meaning that they can loan out the rest of the money. When a bank makes a loan, both the bank and the person who borrows the money count the funds as assets, doubling the original amount in an economic sense. This currency is then re-used, re-invested and re-loaned multiple times, which in turn leads to the multiplier effect, and this is how fractional reserve banking “creates new money”.

Lending and debt are integral to the fractional reserve banking system and often requires a central bank to put new currency into circulation, so commercial banks are able to provide withdrawals. Most central banks also perform as regulatory agencies that determine, among other things, the minimum reserve requirement. Such a banking system is what most countries’ financial institutions use. It’s prevalent in the United States and in numerous other free-trade countries.

The Creation of Fractional Reserve Banking Systems

The fractional reserve banking system was created around 1668 when the Swedish (Sveriges) Riksbank was established as the first central bank in the world - but other primitive forms of fractional reserve banking had already been in use. The idea that money deposits could grow and expand, stimulating the economy through loans, quickly became a popular one. It made sense to use the available resources to encourage spending, rather than hoard them in a vault.

After Sweden took steps to make the practice more official, the fractional reserve structure took hold and spread fast. Two central banks were established in the U.S., first in 1791 and next in 1816, but neither lasted. In 1913, the Federal Reserve Act created the U.S. Federal Reserve Bank, which is now the U.S. central bank. The named objectives of this financial institution are to stabilize, maximize and oversee the economy in regards to pricing, employment, and interest rates.

How does it work?

When a customer deposits money in their bank account, that money is no longer the depositor's property, at least not directly. The bank now owns it, and in return, they give their customer a deposit account that they can draw on. This means their bank customer should have access to their full deposit amount upon demand, with established bank rules and procedures. However, when the bank takes possession of the deposited money, it doesn't hold on to the full amount. Instead, a small percentage of the deposit is reserved (a fractional reserve). This reserve amount typically ranges from 3% to 10% and the rest of the money is used to issue loans to other customers.

Consider how these loans create new money with this simplified example:

- Customer A deposits $50,000 in Bank 1. Bank 1 loans Customer B $45,000

- Customer B deposits $45,000 in Bank 2. Bank 2 loans Customer C $40,500

- Customer C deposits $40,500 in Bank 3. Bank 3 loans Customer D $36,450

- Customer D deposits $36,450 in Bank 4. Bank 4 loans Customer E $32,805

- Customer E deposits $32,805 in Bank 5. Bank 5 loans Customer F $29,525

With a fractional reserve requirement of 10%, that original $50,000 deposit has grown to $234,280 in total available currency, which is the sum of all customers’ deposits plus $29,525. While this is a very simplified example of the way fractional reserve banking generates money via the multiplier effect, it demonstrates the basic idea.

Note that the process is based on the principal of debt. Deposit accounts represent money that banks owe their customers (liability) and interest-earning loans make the most money for banks and they are a bank’s asset. Simply put, banks make money by generating more loan account assets than deposit account liabilities.

What About Bank Runs?

What if everyone who hold deposits in a certain bank decides to show up and withdraw all their money? This is known as a bank run and since the bank is only required to hold up a small fraction of their customers’ deposits, it would likely cause the bank to fail due to an inability to meet their financial obligations.

For the fractional reserve banking system to work, it's imperative that depositors don't descend on the banks to withdraw or access all their deposit amounts simultaneously. Though bank runs have occurred in the past, it's typically not how customers behave. Normally, customers only attempt to remove all their money if they believe the bank is in serious trouble.

In the U.S., the Great Depression is one notorious example of the devastation a massive withdrawal can cause. Today, the reserves held by banks is one of the ways they work to minimize the chance of this happening again. Some banks hold more than the mandated minimum in reserve to better meet their customer demands and provide access to their deposit account funds.

Advantages and Disadvantages of Fractional Reserve Banking

While banks enjoy most of the advantages of this highly lucrative system, a tiny bit of this trickles down to bank customers when they earn interest on their deposit accounts. Governmental are also part of the scheme and often defend that fractional reserve banking systems encourage spending and provide economic stability and growth.

On the other hand, many economists believe that the fractional reserve scheme is unsustainable and quite risky - especially if we consider that the current monetary system, implemented by most countries, is actually based on credit/debt and not on real money. The economic system we have relies on the premise that people trust both the banks and the fiat currency, established as legal tender by the governments.

Fractional Reserve Banking and Cryptocurrency

In contrast with the traditional fiat currency system, Bitcoin was created as a decentralized digital currency, giving birth to an alternative economic framework that works in an entirely different way.

Just like most cryptocurrencies, Bitcoin is maintained by a distributed network of nodes. All data is protected by cryptographic proofs and recorded on a public distributed ledger called blockchain. This means that there is no need for a central bank and there is no authority in charge.

Also, the issuance of Bitcoin is finite so that no more coins will be generated after the max supply of 21 million units is reached. Therefore, the context is totally different and there is no such a thing as fractional reserve in the world of Bitcoin and cryptocurrencies.