Осторожно! Много текста.

- Кредит — деньги, которые предоставляются на время с условием возврата. Кредит питает экономику.

- Увеличение количества кредитов подразумевает увеличение расходов. Большие расходы одних лиц приносят большие доходы другим, в результате чего накапливаются средства для будущих кредитов.

- Кредит неразрывно связан с долгом. Заемные деньги необходимо возвращать, поэтому расходы должны сокращаться.

- Правительства повышают и понижают процентные ставки с целью контролировать экономику.

Введение

Экономика лежит в основе всего. Она влияет на жизнь каждого из нас, и поэтому в ней важно разбираться хотя бы на базовом уровне.

У понятия «экономика» не одно определение, но в широком смысле слова экономику можно описать как область производства, потребления и торговли товарами. Как правило, ее обсуждают на национальном уровне. Каждый день мы слышим об экономике США, Китая и других стран из новостей и репортажей журналистов. Экономическую деятельность также можно рассматривать глобально, принимая во внимание положение дел в каждой конкретной стране.

В данной статье мы рассмотрим составляющие элементы экономики, опираясь на модель Рэя Далио (подробнее об этой модели в видео Как работает экономическая машина).

Из чего состоит экономика

Давайте двигаться от простого к сложному. Каждый день мы все вносим вклад в экономику, покупая (товары) и продавая (свой труд). Все люди, группы, правительства и бизнесы по всему миру покупают и продают в трех секторах рынка.

Первичный сектор занимается добычей природных ресурсов, например лесозаготовкой, сельским хозяйством и добычей золота (и это лишь несколько примеров). Полученные материалы затем используются во вторичном секторе, который отвечает за производство товаров. Наконец, третичный сектор охватывает задачи от рекламы до распространения.

Разделение экономики на три сектора — это общепринятая модель. Однако иногда ее расширяют, добавляя четвертичный и пятеричный сектора, чтобы разграничить услуги в третичном секторе.

Оценка экономической деятельности

Для оценки состояния экономики используются специальные методы, наиболее распространенный из которых — учет ВВП, то есть валового внутреннего продукта. Этот показатель позволяет рассчитать общую стоимость товаров и услуг, произведенных в стране за определенный период.

Рост ВВП указывает на увеличение производства, доходов и расходов, и наоборот — падение ВВП связано с сокращением производства, доходов и расходов. Обратите внимание, что реальный ВВП учитывает инфляцию, а номинальный ВВП — нет.

Хотя ВВП — это лишь приблизительный показатель, он крайне важен для анализа на национальном и международном уровнях. Для оценки экономического состояния стран к его использованию обращаются все — от мелких участников финансового рынка до Международного валютного фонда.

ВВП — это надежный индикатор экономики страны, но, как и в техническом анализе, его лучше сопоставлять с другими данными для получения наиболее полных выводов.

Кредиты, задолженности и процентные ставки

Кредиторы и заемщики

Ранее мы упоминали, что вся экономика сводится к купле-продаже. Однако кредитование и займ также очень важны. Предположим, у вас есть крупная сумма денег, которая в данный момент нигде не используется, и вы решаете использовать эти средства для получения дополнительного дохода.

Один из доступных вариантов — дать их в долг тому, кто нуждается в средствах, например, чтобы купить оборудование для бизнеса. Сейчас у этого человека нет денег, но после покупки оборудования он сможет заработать на продаже своих продуктов и вернет вам долг. В этой ситуации вы выступаете в роли кредитора, а другой человек — в роли заемщика.

Выгода кредитора заключается в комиссии с денег, которые он дает в долг. Предположим, у вас просят в долг $100 000, и вы даете их при условии, что заемщик заплатит вам 1% от этой суммы за каждый месяц до возврата денег. Эта дополнительная плата называется процентами.

В нашем примере заемщик заплатит вам по $1000 за каждый месяц до погашения долга. Если заемщик вернет долг через три месяца, то вы получите $103 000, плюс любые дополнительные комиссии.

Давая деньги в долг, вы создаете кредит — соглашение, по которому заемщик обязуется вернуть средства позже. Пользователи кредитной карты хорошо знакомы с этой концепцией. При оплате картой деньги не снимаются с вашего банковского счета сразу же. Вы можете вовсе не иметь на нем средств, но должны будете оплатить счет позже.

Кредит подразумевает долг. Заемщик должен вернуть деньги кредитору, и его долг будет исчерпан, когда он погасит кредит с процентами.

Банки и процентные ставки

В наше время главные кредиторы — это банки. Эти финансовые учреждения также являются посредниками (или брокерами) между кредиторами и заемщиками, и могут выступать в роли и тех, и других.

Вы кладете деньги в банк при условии, что получите их назад. Другие люди делают то же самое. Поскольку банк располагает такой крупной суммой, он дает ее в долг заемщикам.

Банки не хранят все деньги своих кредиторов. Они работают по системе частичных резервов. Если бы все кредиторы одновременно запросили свои деньги назад, у банка возникли бы проблемы, но это случается крайне редко. В таком случае (например, если люди теряют доверие к банку), происходит банкокая паника, которая может привести к краху банка. Ярчайшие примеры банковой паники происходили в 1929 и 1933 годах во времена Великой депрессии в США.

Банки мотивируют своих клиентов приносить деньги, предлагая процентные ставки. Высокие процентные ставки более привлекательны для кредиторов, поскольку они получат больше денег. Для заемщиков же все наоборот — для них более выгодны низкие процентные ставки.

Важность кредитов

Кредит — это своего рода топливо для экономики. Он позволяет отдельным лицам, бизнесам и даже правительствам тратить деньги, которых у них пока нет в наличии. Некоторые экономисты считают кредиты проблемой, но другие утверждают, что увеличение расходов — это признак процветающей экономики.

Если кто-то тратит деньги, то кто-то другой получает доход. Банки охотнее предлагают кредиты людям с высокими доходами, предоставляя им еще больше денег и кредитов. Чем больше у заемщика денег и кредитов, тем больше трат он совершает, в результате чего больше людей получают доход, и цикл продолжается.

Больше доходов → больше кредитов → больше расходов → больше доходов.

Больше доходов → больше кредитов → больше расходов → больше доходов.

Конечно, этот цикл не может длиться вечно. Взяв взаймы $100 000 долларов, вы должны будете отдать больше, чем $100 000. Хотя ваши расходы увеличатся на время, однажды вам придется сократить их, чтобы вернуть долг.

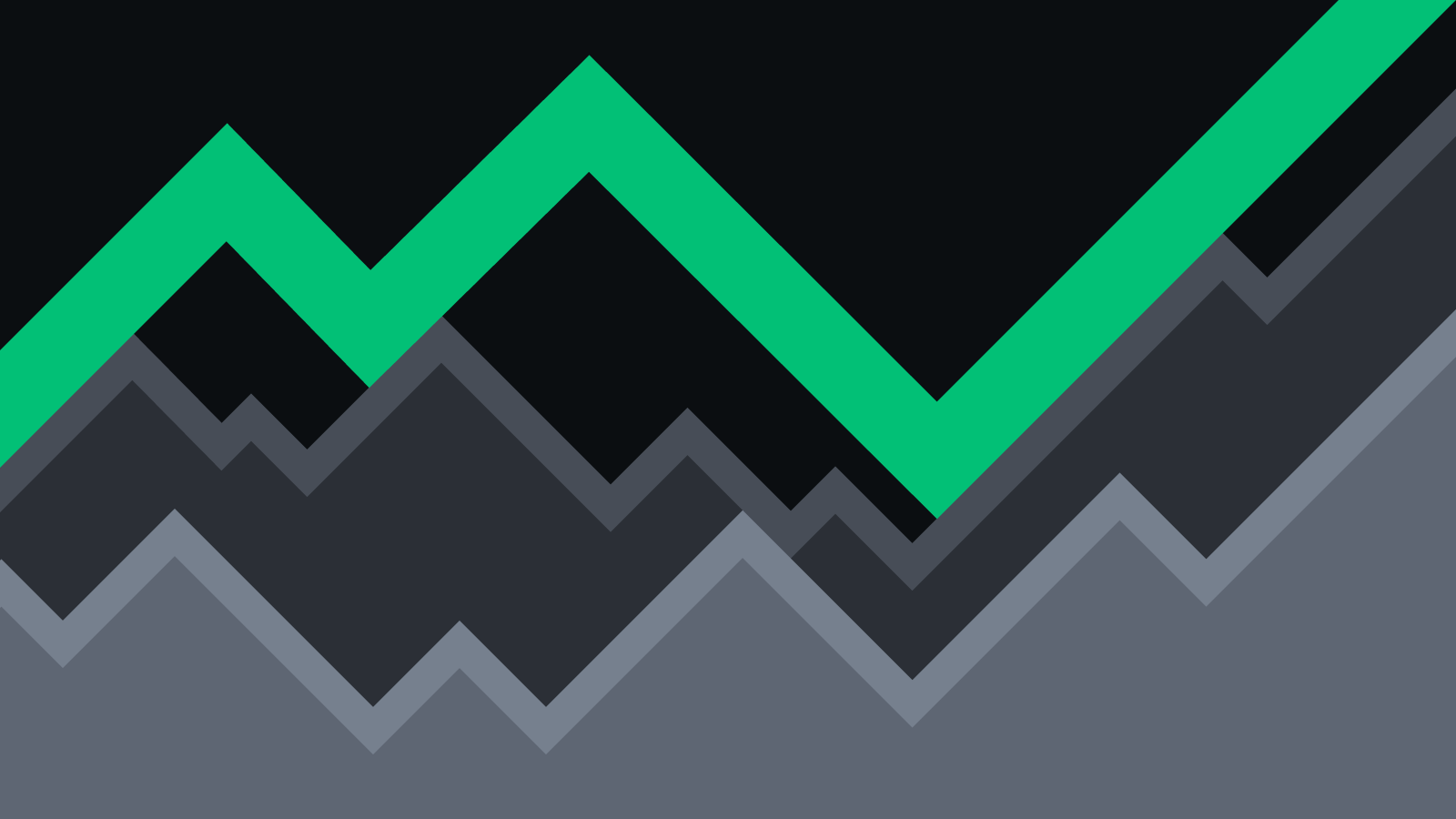

Рэй Далио описывает эту концепцию как краткосрочный долговой цикл. По его оценке, данный цикл повторяется каждые 5-8 лет.

Красным цветом отмечена растущая производительность. Зеленым цветом отмечены объемы доступных кредитов.

Красным цветом отмечена растущая производительность. Зеленым цветом отмечены объемы доступных кредитов.

Давайте разбираться. Прежде всего важно отметить, что производительность неуклонно растет. Без кредита производительность была бы единственным источником экономического роста, так как для получения дохода необходимо производить больше и больше.

В первой части диаграммы мы видим, что из-за кредита доход растет быстрее, чем производительность, что обуславливает экономический рост. В определенный момент рост останавливается, и начинается экономический спад. Во второй части диаграммы доступность кредита значительно снижается после первоначального «бума». Получить кредит становится сложнее, и начинается инфляция, что вынуждает правительство принимать меры по исправлению ситуации.

Мы рассмотрим эту ситуацию подробнее в следующем разделе.

Центральные банки, инфляция и дефляция

Инфляция

Предположим, каждый имеет доступ к большому количеству кредитов (первая часть диаграммы из предыдущего раздела). Взяв кредит, люди смогут приобрести гораздо больше товаров. Расходы стремительно увеличиваются, а производство — нет. Предложение товаров и услуг остается на прежнем уровне, тогда как спрос на них увеличивается.

В результате всего этого случается инфляция: цены на товары и услуги растут из-за высокого спроса. Для измерения инфляции используется индекс потребительских цен (ИПЦ), который отслеживает цены на популярные товары и услуги с течением времени.

Как работает центральный банк

Банки, которые мы упоминали ранее, являются коммерческими банками, которые обычно обслуживают частных лиц и бизнесы. Центральные банки — это государственные органы, отвечающие за управление денежно-кредитной политикой страны. Среди таких учреждений можно выделить Федеральную резервную систему США, Банк Англии, Банк Японии и Народный банк Китая. Центральные банки выполняют такие функции, как увеличение количества денег в обращении (путем количественного смягчения) и контроль процентных ставок.

Центральные банки прибегают к повышению процентных ставок, когда инфляция выходит из-под контроля. С повышением ставок повышаются проценты, поэтому займы становятся менее выгодными. Поскольку физическим лицам также необходимо погашать долги, расходы будут сокращаться.

В идеальном мире высокие процентные ставки приводили бы к снижению цен из-за падения спроса, однако на практике они могут привести к дефляции и другим проблемам.

Дефляция

По названию можно догадаться, что дефляция — это антоним инфляции. Это понятие описывает общее снижение цен за определенный период времени, обычно связанное с уменьшением расходов. Уменьшение расходов, в свою очередь, может сопровождаться рецессией.

Одно из возможных решений дефляции — это снижение процентных ставок. Снижая проценты по кредиту, банки мотивируют людей брать больше займов. С большей доступностью кредитов ожидается, что расходы в разных секторах экономики также возрастут.

Как и инфляцию, дефляцию можно измерить с помощью индекса потребительских цен.

Что случится, когда экономический пузырь лопнет

Согласно Далио, диаграмма, которую мы рассматривали выше (краткосрочный долговой цикл) — это лишь краткий период в рамках долгосрочного долгового цикла.

Долгосрочный долговой цикл

Долгосрочный долговой цикл

Описанная выше модель (увеличение и уменьшение доступности кредита) повторяется с течением времени, однако в конце каждого цикла долги только возрастают. В конце концов это приводит к масштабному сокращению доли заемных средств (когда люди пытаются уменьшить свои долги). На графике это проиллюстрировано внезапным уменьшением.

При сокращении доли заемных средств доходы начинают падать, а доступность кредита снижается. Не имея возможности погасить долг, люди начинают продавать свои активы, но так как многие делают то же самое, цены на активы падают.

Все это приводит к краху фондовых рынков, и на данном этапе центральный банк больше не может снижать процентные ставки, которые уже находятся на уровне 0%. При дальнейшем снижении возникали бы отрицательные процентные ставки, что является спорным и неэффективным решением. Так что же делать? Самый очевидный вариант — сократить расходы и простить долги. Однако это приведет к другим проблемам: сокращение расходов спровоцирует сокращение прибыли бизнесов, а значит и доходов сотрудников. Предприятиям придется сокращать рабочую силу, что приведет к росту безработицы.

Из-за низких доходов и меньшей численности рабочей силы правительство не сможет собирать достаточно налогов, которые необходимы для обеспечения безработных граждан. Правительство, расходуя больше, чем получает, столкнется с дефицитом бюджета.

Одно из возможных решений — начать печатать деньги (прямо как в англоязычном меме money printer go brrrrr, популярном в криптовалютных кругах). Центральный банк сможет одолжить эти деньги правительству, чтобы стимулировать экономику, однако и это может привести к проблемам.

Печать ничем не подкрепленных денег приводит к инфляции из-за увеличения средств. Это опасное развитие событий, которое со временем может перерасти в гиперинфляцию — ситуацию, когда валюта обесценивается, что приводит к экономической катастрофе. Гиперинфляция происходила в 1920-х годах в Веймарской республике, в Зимбабве в конце 2000-х и в Венесуэле в конце 2010-х. По сравнению с краткосрочными циклами долгосрочный долговой цикл длится гораздо дольше и повторяется каждые 50–75 лет.

Как все это связано

Выше мы затронули немало важных вопросов. В конечном итоге модель Далио базируется на доступности кредита: чем больше кредитов, тем лучше состояние экономики, и наоборот. Периоды доступности и недоступности чередуются, создавая краткосрочные долговые циклы, которые являются частью долгосрочных долговых циклов.

Процентные ставки сильно влияют на поведение субъектов экономики. При высоких процентных ставках люди склонны копить деньги, а при низких — расходовать.

Резюме

Экономика — это огромный сложный механизм, разобраться в котором очень тяжело. Однако мы можем выделить определенные тенденции и закономерности, повторяющиеся снова и снова по мере взаимодействия субъектов экономики.

Мы надеемся, что помогли вам разобраться во взаимоотношениях кредиторов и заемщиков и понять важность кредита и долга, а также продемонстрировали, какие шаги предпринимают центральные банки, чтобы смягчить сложные экономические ситуации.