Осторожно! Много текста.

Скорее всего, вы встречали термины APY и APR, когда изучали продукты децентрализованных финансов (DeFi).

Годовая процентная доходность (APY) учитывает проценты, начисляемые ежеквартально, ежемесячно, еженедельно или ежедневно, а годовая процентная ставка (APR) — нет. Это простое различие может существенно изменить вычисление возвратов за определенный период. Поэтому важно понимать, как рассчитываются эти два показателя и как они влияют на доход от цифровых средств.

APR и APY

APR и APY — ключевые понятия для личных финансов. Начнем с более простого термина — годовой процентной ставки (APR). Это процент, который кредитор зарабатывает на своих деньгах в течение одного года, при этом оплачивает его заемщик.

Например, если вы положите $10 000 на сберегательный счет в банке с APR 20%, то через год вы заработаете $2 000 в виде процентов. Они рассчитываются путем умножения основной суммы ($10 000) на ставку APR (20%). Таким образом, через год у вас будет $12 000. Через два года — $14 000. Через три года вы накопите $16 000, и так далее.

Прежде чем перейти к годовой процентной доходности (APY), разберемся, что такое сложные проценты. Проще говоря, это получение процентов за предыдущие проценты. Если финансовое учреждение в примере выше выплачивает проценты на ваш счет ежемесячно, ваш баланс будет выглядеть по-разному в течение каждого из двенадцати месяцев года.

Вместо того, чтобы получить $12 000 долларов в конце двенадцатого месяца, вы будете получать часть процентов каждый месяц. Эти проценты добавляются к основной сумме вашего депозита, поэтому сумма, от которой вы получаете проценты, растет с каждым месяцем. С каждым месяцем ваш заработок будет увеличиваться. Так работает сложный процент.

Допустим, вы положили $10 000 на банковский счет с APR 20%, и проценты начисляются ежемесячно. Если не вдаваться в сложную математику, то в конце года вы получите $12 429. Это на $429 больше просто за счет сложных процентов. Сколько вы бы заработали при ставке APR 20% и ежедневном начислением процентов? Всего вы бы получили $12 452.

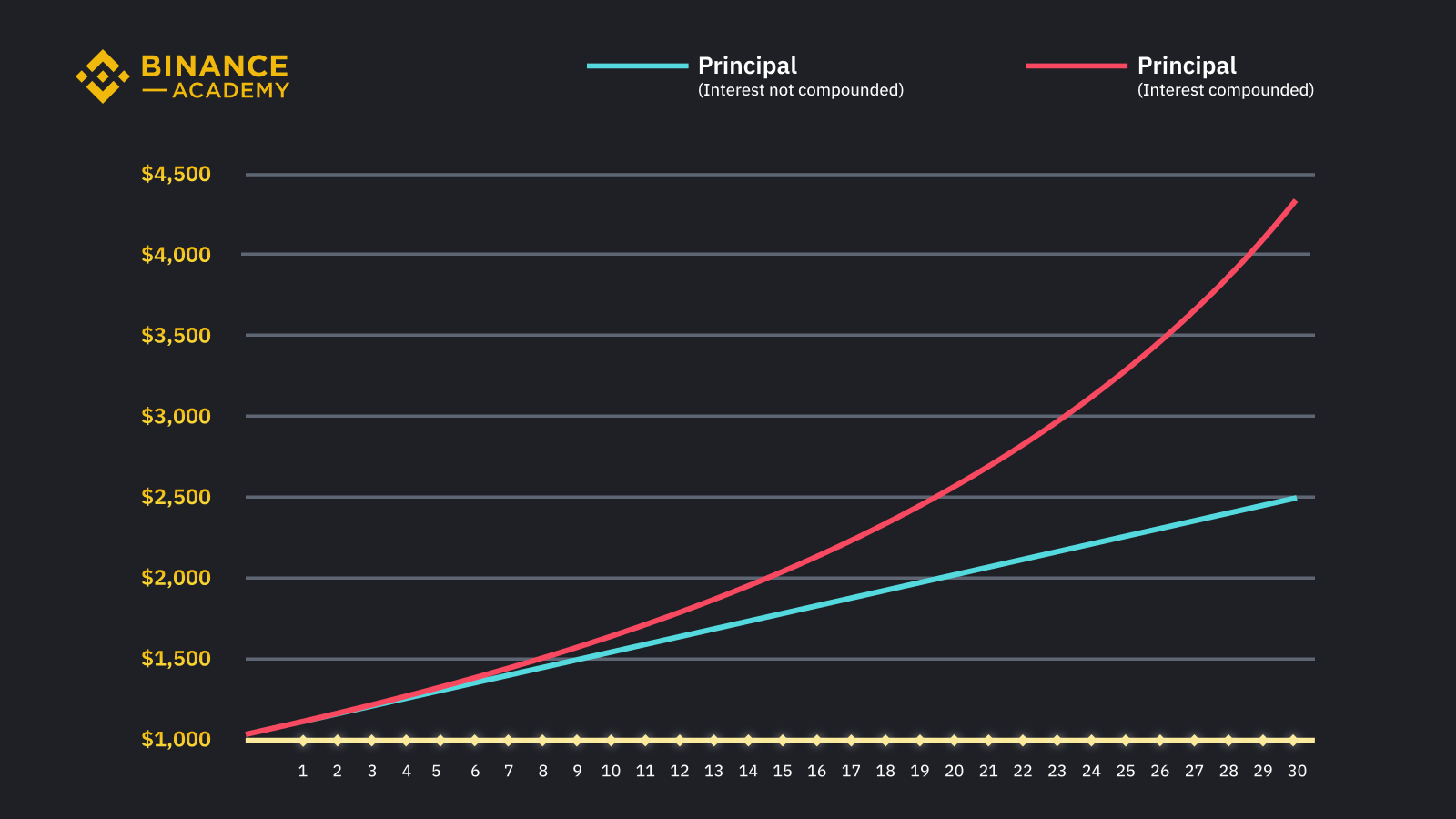

Эффект сложного процента лучше всего заметен в длительные периоды времени. Те же APR 20% с ежедневным процентом через три года принесет $19 309. Это на $3 309 больше, чем по тому же продукту с APR 20% без сложного процента.

Добавив сложный процент, вы заработаете на своих вложениях гораздо больше. Обратите внимание, что проценты различаются в зависимости от частоты начисления: чем чаще, тем больше заработок. Ежедневное начисление принесет больше процентов, чем ежемесячное.

Как же рассчитать доход от продукта со сложным процентом? Вот тут-то и приходит на помощь годовая процентная доходность (APY). Используйте специальную формулу, чтобы конвертировать APR в APY с учетом частоты начисления. Например, APR 20% с ежемесячным начислением равняется 21,94% APY. При ежедневном начислении она составит 22,13% APY. Эти цифры представляют собой годовой процентный доход, который вы получаете после учета сложных процентов.

В целом, APR (годовая процентная ставка) проще и статичнее: она остается фиксированной. Но APY (годовая процентная доходность) включает процент, начисляемый на процент, то есть сложный процент. Она изменяется в зависимости от частоты начисления. Чтобы выучить разницу, запомните, что «доходность» — более сложная концепция (и более прибыльная).

Как сравнить процентные ставки?

Из примера выше видно, что при сложении процентов можно получить больше процентов. Ставки различных продуктов могут быть в виде APR или APY. Из-за этого различия важно использовать для сравнения один и тот же термин. Будьте внимательны при сравнении продуктов, поскольку вы можете сравнивать яблоки с апельсинами.

Продукты с более высокой APY не обязательно будут приносить больше процентов, чем продукты с более низкой APR. Вы можете легко конвертировать APR и APY с помощью онлайн-инструментов, если знаете частоту начисления.

То же самое касается DeFi и других видов криптопродуктов. При рассмотрении продуктов с криптовалютными APY и APR, таких как криптовалютные депозиты и стейкинг, обязательно конвертируйте их, чтобы сравнивать яблоки с яблоками.

Кроме того, сравнивая два продукта DeFi по APY, убедитесь, что у них одинаковые периоды начисления. Если у них одинаковый APR, но один рассчитывается ежемесячно, а другой ежедневно, то ежедневный вариант может принести больше криптовалютных процентов.

Еще один важный момент, на который следует обратить внимание, — это значение APY для конкретного криптопродукта, который вы рассматриваете. В некоторых продуктах термин «APY» используется для обозначения вознаграждения, которое можно заработать в криптовалюте за выбранный период времени, а не фактического или прогнозируемого дохода/доходности в любой фиатной валюте. Это важное различие, поскольку цены на криптоактивы могут быть нестабильными, и стоимость ваших инвестиций (в фиатном выражении) может как упасть, так и вырасти. Если цены на криптоактивы резко упадут, стоимость ваших инвестиций (в фиатном выражении) может оказаться ниже первоначальной фиатной суммы, которую вы вложили, даже если вы продолжите зарабатывать APY в криптоактивах. Поэтому важно изучить правила и условия продукта и провести собственное исследование, чтобы разобраться в инвестиционных рисках и что APY означает в конкретном контексте.

Резюме

APR и APY поначалу могут путать, но их легко различать, если помнить, что годовая процентная доходность (APY) — это более сложная метрика со сложными процентами. Из-за начисления процентов на проценты APY всегда выше, если проценты начисляются чаще, чем раз в год. Всегда проверяйте ставку продукта при расчете процентов, которые вы заработаете.